How Much Do You Have to Make to Be in the 1

Expect to need at least $100K of income for a $1M home

There's no magic formula that says you need x income to afford a $1 million house. Because income is just part of the equation.

With a really strong financial profile – high credit, low debts, big savings – you might afford a $1 million home with an income around $100K.

But if your finances aren't quite as strong, you might need an income upwards of $225K per year to buy that million–dollar home.

Wondering how much house you can afford? Here's how you can find out.

Verify your home buying budget (Dec 5th, 2021)In this article (Skip to...)

- Income to afford a million dollar home

- Calculate your home buying budget

- Don't forget about homeownership costs

- Benefits of buying a $1M house

- Today's mortgage rates

Income to afford a million–dollar home

As we said above, income is just one factor in your home buying budget.

The purchase price you can afford also depends on your:

- Debt–to–income ratio (DTI)

- Credit score

- Down payment amount

- Mortgage rate

We experimented with a few of these factors using our home affordability calculator to show you how much each one can affect your budget.

Prime borrower – $147,000 income needed

Our first example looks at a traditional 'prime' borrower. They have:

- A 20% down payment ($210,000)

- Only $250 in pre–existing monthly debts

- An excellent mortgage rate of 2.75%

This borrower can afford a $1 million dollar house with a salary of $147,000. Their monthly mortgage payment would be about $4,100.

High DTI – $224,000 income needed

Let's leave everything else the same as in the first example, but increase the borrower's monthly debt payments to $2,500.

For those paying multiple child support and alimony payments, that might be more realistic, even if their debts are only average.

And others have that level of debt payment even without family commitments. Think luxury car, boat, motorhome, and other big–ticket toys.

In this scenario, the income needed to afford a home costing 1.031 million would be $224,000.

To afford this home, you'd need a slightly higher down payment of $214,000. And monthly payments would cost about $4,220.

Clearly, existing debts make a big difference in home affordability. Your salary needs to be $77,000 higher to buy a similarly–priced home.

Lower credit – $224,000 income needed

In most cases, a million–dollar purchase price will require a jumbo loan.

To get a jumbo loan, you typically need a credit score of 700 or higher. But let's say a borrower has a credit score on the lower end of the approvable range.

Lower credit means they'll have to pay a higher interest rate than our earlier example. We'll say 3.0% instead of the 2.75% used earlier.

That same $224,000 income will still buy a $1 million home, though the budget comes in at one at $1,005,000 rather than $1,031,000 – a full $25,000 lower.

And that's still assuming $2,500 in monthly debt payments.

Let's say you can afford a 50% down payment. Perhaps you've built up lots of equity as a long–standing homeowner. Or maybe you've had a windfall.

Chances are, in your happy financial position, you've paid down most of your debt, so we'll return that number to $250 a month.

By putting down half the purchase price ($500,000) you can afford a $1 million home on an income of just $110,000.

Even putting down 30% makes a big difference compared to 20%.

With 30% down, you could potentially afford a $1,037,000 home on an income of $140,000. Compare that with needing an income near $150,000 if you put down only 20%.

How to calculate your home buying budget

The best way to figure out your home buying budget – short of contacting a lender – is to use a mortgage calculator.

This mortgage calculator will help you figure out how much house you can afford based on your salary, down payment, and debts. It also accounts for other factors, like your mortgage interest rate and estimated property taxes and homeowners insurance costs.

To get the best estimate, be as accurate as you can when filling out each field.

- Annual income – Your gross income from all sources before tax

- State – Your location can affect the deal you'll get. And it will also impact your property taxes

- Monthly debts – Minimum card payments, plus loan installments, plus alimony and child support. In other words, all your inescapable, monthly financial obligations. But not things that vary, such as food, gas, utilities, and so on

- Loan term – Are you using a 30–year fixed–rate mortgage loan or a 15–year fixed–rate loan? This will have a big impact on how much house you can afford

- Interest rate – You won't know your mortgage rate for sure until you get loan estimates from multiple lenders. The default shown on our calculator is an average rate on the day you visit; yours will be higher or lower, depending mainly on your credit, down payment, and debt burden. So adjust as best you can

- Down payment – Your down payment affects your interest rate as well as your overall homebuying budget. Assume you'll need at least 20% of the purchase price to get approved for such a big loan

- Other homeownership costs – Estimate your future homeowners insurance premiums and property taxes. The numbers in the calculator are state averages. And add in monthly homeowners association dues, if you're buying in an HOA's area

Remember, a calculator can only give you an estimate. To know whether you can really afford a $1 million home, you'll need to get pre–approved by a mortgage lender.

Pre–approval means the lender has verified your credit, income, savings, and other items on your application.

If you have a pre–approval letter in hand stating you can afford a million–dollar home, then it's more or less a sure thing. (Unless any of your financials or mortgage rates change substantially prior to purchase.)

Start your mortgage pre-approval (Dec 5th, 2021)Don't forget about homeownership costs

So far, we've only looked at the purchase price for a million–dollar house.

We've explored the principal (repaying the sum you borrowed) and interest on your mortgage. And we've taken into account your likely property taxes and homeowners insurance.

But there are plenty of other costs associated with owning a home – especially with high–value real estate. And you'll need to budget for these as well.

Closing costs

People often think about their home buying budget in terms of down payment. For a $1 million home, you're likely to need a minimum of $100,000 to $200,000 saved up in that department.

But a down payment isn't the only thing to save for. Home buyers have to consider closing costs on their home purchase, too.

Closing costs typically start around 2% of the buyer's loan amount.

So if you're borrowing $800,000 to buy a million dollar house, your closing costs could be around $16,000 or more. You'll need to factor this number in when thinking about how far your savings will stretch.

Property taxes and homeowners insurance

Home buyers also need to consider their future property taxes.

Real estate tax rates are set by local tax authorities, and they vary a lot depending on where you live.

But to give you a ballpark estimate, the average national property tax rate is around 1 percent.

That means on a $1M house, there's a good chance you could pay around $10,000 per year in property taxes. That's over $800 per month.

Research property tax rates where you plan to buy and make sure you factor this cost into your budget for ongoing housing costs.

Homeowners insurance is likely to be more expensive on a larger home, too. The typical homeowner might spend $50 to $75 per month to insure a standard home.

But a larger home costs more to replace if it is destroyed by fire or other disaster. Naturally, the insurance company will charge more for greater risk.

Expect to pay $100 to $200 per month to insure your million–dollar home.

All in, you'll likely pay $1,000 per month in taxes and insurance, a sizeable bill above and beyond the principal and interest payment.

Running costs, repairs and maintenance

The bigger your home, the more it costs to run. The larger square footage and perhaps higher ceilings that you loved, mean you have a larger volume to heat and cool. So your utility and HVAC servicing bills are going to be a lot higher.

A bigger home also means more to clean and maintain – and often comes with a yard that will require upkeep.

In short, keeping a large home well maintained isn't cheap. And neither are repairs. So plan ahead and make sure your home buying budget leaves you with a sizeable cushion in your savings account.

Benefits of buying a $1M house

Your ongoing costs may be higher with a bigger home. But the benefits to your net worth should typically be greater, too.

Indeed, home price appreciation jumped to a six–year high over the 12 months ending in September 2020, according to CoreLogic.

During that time, CoreLogic says home values increased 6.7% year over year.

That means if your home were worth $325,000, you'd have added a handsome $21,775 to your net worth that year on average.

And for a million–dollar home? Prices were up by nearly $70,000 year–over–year. So you're likely to see a nice return on the money you invest in your house.

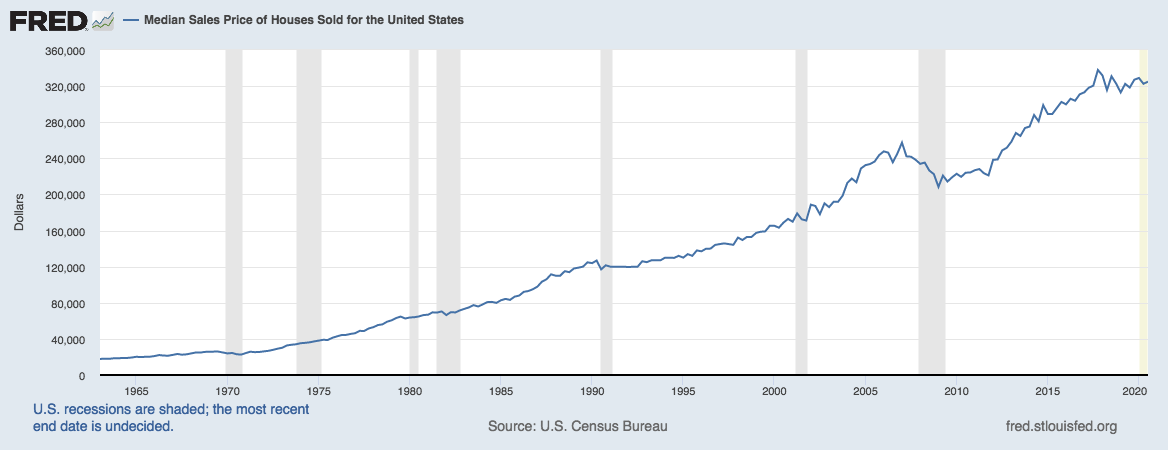

Of course, all this relies on home prices continuing to rise. And we all know that they very occasionally fall.

But take a look at this graph from the Federal Reserve Bank of St. Louis:

Source: U.S. Census Bureau and U.S. Department of Housing and Urban Development, Median Sales Price of Houses Sold for the United States

You can see how rare it is for home values to decrease – and how strong the overall upward trend is.

You might think real estate is not a bad place to have $1 million invested.

Today's rates are helping home buyers

There's one other trend prospective home buyers should pay attention to, and that's mortgage rates.

Low mortgage rates boost affordability. And today's rates are sitting near record lows.

So if you're in the market for a high–priced home, it's a good time to be looking at financing.

Show me today's rates (Dec 5th, 2021)The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

How Much Do You Have to Make to Be in the 1

Source: https://themortgagereports.com/71443/income-to-afford-1-million-dollar-house